No, you do not need insurance for urgent care. While having a health plan can definitely cut your costs, almost every urgent care center is happy to see patients who prefer to pay for their visit directly.

Understanding Your Urgent Care Payment Options

Let's say a nasty sinus infection hits you on a Friday night. Do you have to have an insurance card to get seen? Not at all. Urgent care clinics are built for accessibility.

Think of it like grabbing a coffee: you can pay with a pre-loaded gift card (your insurance) or just use your debit card (self-pay). Either way, you get the same great coffee. It works the same way with urgent care—both payment methods get you the same quality medical care.

This flexible model makes these clinics a lifeline for a lot of people. In fact, one national survey found that about 12.1% of all urgent care visits were from patients paying themselves or without insurance. That's a huge number of people getting care without needing a policy. You can read more about these trends in the full findings on urgent care accessibility.

Before we dive deeper, here's a quick look at how the main payment options stack up.

Urgent Care Payment Options at a Glance

| Payment Method | How It Works | Best For |

|---|---|---|

| Using Insurance | The clinic bills your insurance company. You pay your copay or a portion of the bill after your deductible. | Patients with an active insurance plan who want to keep out-of-pocket costs low for covered services. |

| Self-Pay (Cash Pay) | You pay the clinic's listed price directly at the time of your visit, often with cash, a credit card, or a debit card. | Anyone without insurance, those with high-deductible plans, or people seeking services not covered by their policy. |

| Telemedicine Service | You pay a flat fee for a virtual consultation for common issues, bypassing traditional clinic visits entirely. | People with non-emergency conditions who want a fast, low-cost, and convenient alternative to an in-person visit. |

This table gives you a clear snapshot, but let's break down what these choices mean for you and your wallet.

Insured vs. Self-Pay Visits

When you walk in with an insurance card, the clinic sends the bill to your provider. You’ll usually cover a smaller, predictable amount like a copay.

If you're paying yourself, you cover the clinic’s self-pay rate on the spot. This route is often refreshingly simple. You know the exact cost upfront, with no surprise bills showing up in the mail weeks later after an insurance claim is processed.

Many clinics even offer a “prompt-pay” discount if you settle the bill right then and there because it saves them a ton of administrative work. That kind of flexibility is a core part of what makes the urgent care model so valuable.

Urgent care centers bridge the gap between your primary care doctor and the emergency room, offering a convenient and affordable path to treatment for non-life-threatening issues, regardless of your insurance status.

Whether you're insured, underinsured, or just paying out of pocket, you have a clear path to getting the medical attention you need. Understanding these options is the first step toward making a confident and cost-effective healthcare decision.

And now, modern alternatives like telehealth are expanding your choices even further, offering low-cost care right from the comfort of your home.

How Your Insurance Works at Urgent Care

Walking into an urgent care clinic with your insurance card can feel a little intimidating. What are you actually going to pay? The good news is that it’s usually more straightforward than you think. Think of your insurance plan as a financial partner for your health. When you visit a clinic, you’re not just a patient—you’re activating that partnership.

The whole process kicks off the moment you check in. You’ll hand over your insurance card, and the front desk staff will verify your coverage. Their main goal here is to confirm that the clinic is in-network, meaning they have a pre-negotiated rate with your insurance company. This is the single most important step to keeping your costs as low as possible.

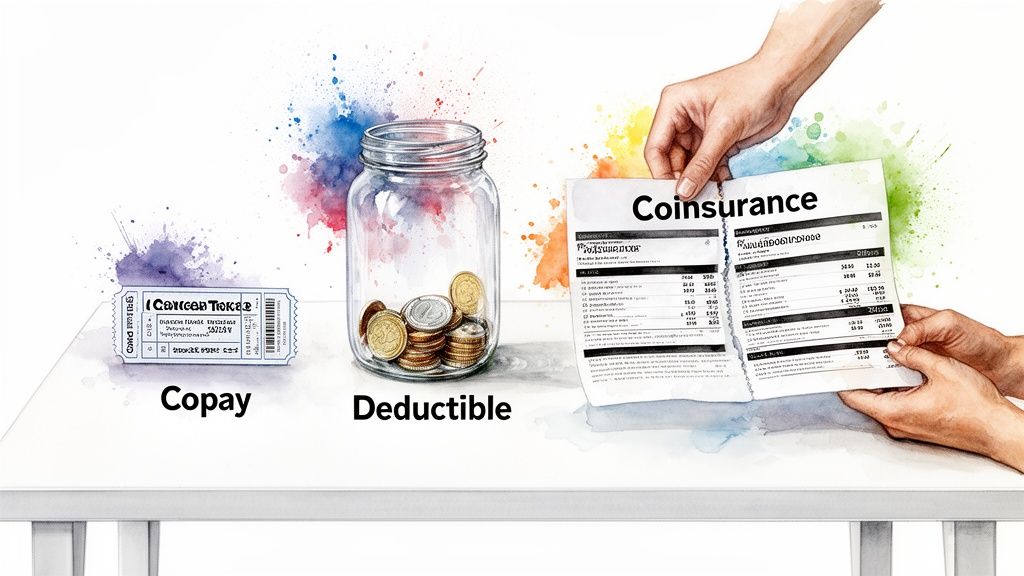

Decoding Your Insurance Terms

To really get a handle on your potential costs, you just need to know three key terms. They're the building blocks of how you and your insurance company share the bill.

Copay: This is your entrance fee. It’s a fixed, predictable amount you pay right at the start of your visit, like a $25 or $50 cover charge. You can usually find this amount printed right on your insurance card.

Deductible: This is the amount you have to pay out-of-pocket for your healthcare each year before your insurance company starts chipping in more significantly. If your plan has a $1,000 deductible, you're responsible for the first thousand dollars of your medical bills.

Coinsurance: Once you've paid your full deductible for the year, you move into a cost-sharing phase. Coinsurance is the percentage of the final bill you’re responsible for. A common split is 20/80, where you pay 20% and your insurer handles the other 80%.

These three pieces work together to figure out your final bill. And remember, not all insurance is the same. Before you find yourself in a tricky spot, it's worth understanding the key differences between travel and health insurance, because your regular plan might not cover you in every situation.

What to Expect After Your Visit

Once you've been treated and are on your way, the urgent care clinic gets to work. They’ll send a claim—basically an itemized bill for everything they did—to your insurance company.

Your insurer then reviews that claim, checks it against your plan's benefits, and figures out how much they will pay based on whether you've met your deductible and what your coinsurance rate is.

Next, you'll get a document in the mail or in your online portal called an Explanation of Benefits (EOB). This is not a bill. It's a detailed breakdown that shows what the clinic charged, what your insurance paid, and what you still owe.

Finally, the urgent care center will mail you a bill for the remaining balance. This could be anything from your copay (if you didn't pay it upfront) to the amount that went toward your deductible or your coinsurance percentage.

Understanding this flow takes the mystery out of the process, helping you anticipate your final costs. Of course, you can sidestep a lot of this complexity with virtual services. You can learn more about our online urgent care for a simple and convenient alternative.

Paying for Urgent Care Without Insurance

For millions of Americans, the thought of walking into a clinic without an insurance card is a stressful one. But when it comes to urgent care, paying directly out-of-pocket—often called self-pay or cash-pay—is not only common but surprisingly straightforward. It cuts through all the red tape of insurance claims and often gives you a much clearer idea of what you’ll actually owe.

Here’s the thing: when you pay upfront, the clinic gets to skip the administrative headache of billing an insurance company, fighting for approvals, and chasing down payments. That saves them real time and money, and many are more than happy to pass some of those savings on to you. This is why you’ll often find lower "self-pay" rates or see a "prompt-pay" discount offered.

What to Expect with Self-Pay Prices

Without insurance, the cost boils down to the specific services you need. A basic visit for something simple will cost a lot less than one that needs tests or a procedure. Prices definitely vary depending on where you live and which clinic you choose, but you can use these numbers as a general ballpark.

Here are some typical self-pay price ranges for common urgent care visits:

- Basic Visit (Consultation): $100 – $250 for things like a cold, sinus infection, or a mild rash.

- Strep Throat Test: The visit plus the lab test will likely run between $150 – $300.

- Minor Sprain (with X-ray): For the exam, imaging, and something like a brace, expect to pay between $250 – $450.

The huge growth in urgent care is a direct answer to the need for medical options that are both accessible and affordable. The number of centers in the U.S. jumped from 8,774 in 2018 to 9,279 in 2019, and that trend hasn't slowed down. This boom provides a critical alternative to insanely expensive emergency room visits, which added up to a staggering $76.3 billion in 2017 alone. Even without insurance, tons of people rely on these clinics; studies show that 19.3% of uninsured children visited an urgent care or retail clinic in 2019. If you want to dig into the numbers, you can explore the data on urgent care and ER affordability.

How to Manage Your Costs

Being a self-pay patient puts you in the driver's seat. You have the power to ask questions, shop around, and make sure you’re getting good value for your money. You don’t need insurance for urgent care, but you do need to be a savvy consumer.

By paying directly, you shift from being a passive participant in a complex billing system to an active customer purchasing a specific service. This mindset is key to controlling your healthcare spending.

Here are three simple, practical steps you can take to keep costs down and avoid any nasty surprises when paying without insurance:

- Ask for a Price List: Before you agree to anything, just ask the front desk for a list of their prices for common services. Any transparent clinic should have no problem giving you one.

- Inquire About Discounts: Always, always ask if they offer a "prompt-pay" or "cash-pay" discount. Many clinics will knock 10-30% off the bill if you can pay in full right then and there.

- Compare Local Clinics: If your situation isn’t a true emergency, take five minutes to call two or three local urgent care centers. A quick phone call can uncover big price differences for the exact same service.

Urgent Care Versus the Emergency Room Cost Comparison

Trying to decide between urgent care and the emergency room can feel like a high-stakes guessing game, but once you understand the massive difference in cost and purpose, the choice becomes much clearer.

Think of it this way: the ER is like a five-star, all-inclusive resort. It's built to handle absolutely any medical crisis you can imagine, from a heart attack to a major car accident. But you pay a massive premium for that round-the-clock readiness, even if all you need is a simple fix.

In contrast, urgent care is more like a high-quality business hotel. It's efficient, perfectly equipped for common and pressing issues, and costs a tiny fraction of the price. The financial gap isn't just a little difference—it's often staggering.

The Financial Impact of Your Choice

The huge price difference really boils down to one thing: facility fees. Emergency rooms are legally required to maintain a massive infrastructure to handle life-or-death situations 24/7, and those enormous operational costs get passed on to every single patient who walks through their doors. An urgent care clinic, on the other hand, has much lower overhead.

This means that for the exact same medical problem, the final bill can be astronomically different.

A visit to the ER for something as common as bronchitis could easily run you over $1,000. Head to an urgent care center for the same diagnosis and treatment, and you might only pay around $150. That’s not a small savings; it's a financial decision that can save you hundreds, or even thousands, of dollars.

For a deeper dive into how these facilities stack up, especially after an accident, check out this article on Urgent Or Emergency Care After An Accident Which Is Better.

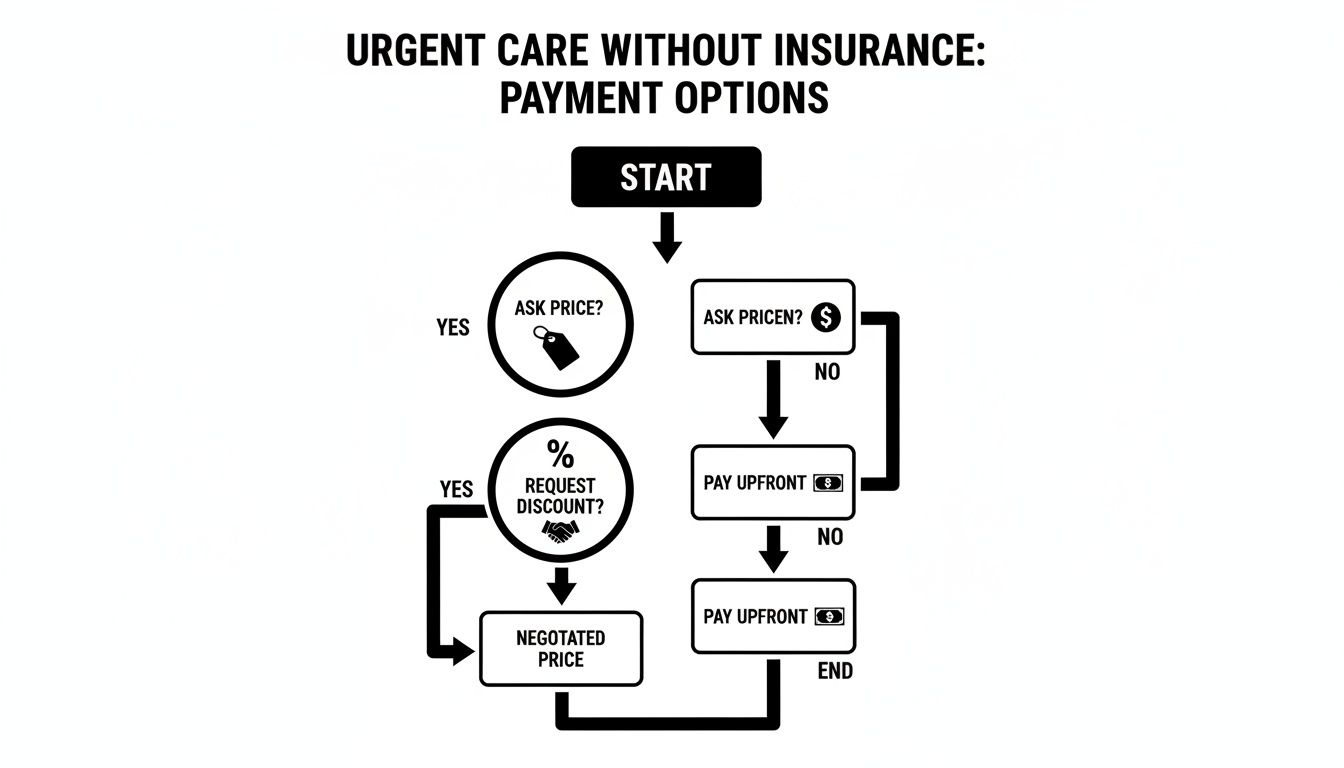

If you're paying out-of-pocket, the path to managing costs at an urgent care clinic is pretty straightforward. This chart breaks down the simple steps you can take.

As you can see, a self-pay patient can take control by confirming prices upfront and asking about prompt-pay discounts before ever handing over a credit card.

Urgent Care vs Emergency Room When to Choose Which

Making the right choice is crucial for both your health and your wallet. It all hinges on how severe your symptoms are. Urgent care is the smart, cost-effective option for issues that are pressing but not life-threatening. The ER is reserved for true medical emergencies where a life or limb is at risk.

This table is a quick guide to help you make the right call in the moment.

| Factor | Urgent Care | Emergency Room (ER) |

|---|---|---|

| Typical Conditions | Colds, flu, minor cuts, sprains, UTIs, mild asthma, rashes | Chest pain, stroke symptoms, severe bleeding, head injuries, major broken bones |

| Average Cost | $100 – $250 (self-pay) | $1,000+ (often much higher) |

| Average Wait Time | Under 1 hour | Can be several hours, depending on triage |

| Severity Level | Pressing but not life-threatening | Life-threatening or limb-threatening emergencies |

| Best For | Getting fast, affordable care for common illnesses and injuries. | Immediate treatment for severe, complex, or dangerous medical conditions. |

Ultimately, the best way to decide is to ask yourself one simple question: "Is this life-threatening?"

If the answer is no, choosing urgent care will get you the exact care you need without the extreme costs and agonizingly long wait times of an ER. This is especially true if you’re paying out-of-pocket, as the lower baseline price makes it a much more manageable option.

A Smarter Alternative: Modern Telehealth Services

What if you could skip the crowded waiting room, the commute, and the confusing medical bills entirely? Modern telehealth platforms have stepped up as a powerful solution, putting expert medical care right on your phone or computer. It’s a huge shift from the old clinic model, giving you direct control over convenience and cost.

This approach is a lifesaver for common, non-emergency issues. Instead of blowing up your schedule for an in-person appointment, you can connect with a doctor from literally anywhere. It’s especially clutch when you need fast treatment for things like a urinary tract infection (UTI), a sinus infection, or pink eye.

The Power of a Simple Flat Fee

Probably the single best thing about services like ChatWithDr is the crystal-clear pricing. For a flat fee of $39.99, you get a complete consultation with a board-certified physician. That one payment covers it all—the diagnosis, a personalized treatment plan, and a prescription sent to your pharmacy if you need one.

That kind of clarity completely removes the financial stress that usually comes with getting medical care. You know the exact cost before you even start the conversation, with zero risk of a surprise bill showing up in the mail weeks later. It's a simple, predictable way to handle your medical costs.

With telehealth, you’re not just paying for a consultation; you’re investing in a streamlined healthcare experience that values your time and your budget. It’s care on your terms, available 24/7.

This model is a game-changer whether you have insurance or not. If you’re uninsured, it's almost always cheaper than a self-pay urgent care visit, where the bill can easily start at over $100 just to walk in the door. And if you have a high-deductible plan, paying a flat $39.99 out-of-pocket can actually be more affordable than using your insurance and dealing with copays and deductibles.

How Text-Based Care Works for You

Platforms like ChatWithDr have also fine-tuned the consultation process to be as convenient as possible. By using a text-based system, they get rid of the need for awkward video calls, letting you talk to a doctor discreetly and efficiently on your own time.

This simple process is perfect for a huge range of needs:

- Treating Common Illnesses: Get quick, effective care for issues like bronchitis, sore throats, or ear infections.

- Managing Chronic Conditions: Easily request refills for your ongoing medications without the hassle of an in-person visit.

- Addressing Sensitive Issues: Discuss personal health concerns like sexual health or hair loss privately and securely.

By moving the entire point of care online, these services make it easier than ever to get professional medical advice. You can check out a full list of telehealth services to see how they can fit into your life. The whole experience is designed around your schedule, giving you access to top-tier medical professionals without the usual headaches of in-person healthcare. It’s a modern solution for modern health needs.

Your Urgent Care Questions Answered

Even when you know the basics, real-life questions always pop up when you're in the middle of a medical issue. Think of this section as your quick-reference guide for those common "what if" moments. We've pulled together the questions we hear most often to give you direct, practical answers.

Our goal is to get ahead of your concerns and give you clear, actionable advice. That way, you'll feel more confident and prepared, whether you’re using insurance, paying cash, or trying out a telehealth option.

Using Tax-Advantaged Health Funds

One of the smartest ways to handle medical costs is with pre-tax money you’ve already set aside. This is where accounts like HSAs and FSAs are a game-changer. But do they work for urgent care?

Can I use my HSA or FSA card for a self-pay urgent care visit?

You absolutely can. An urgent care visit is a qualified medical expense, meaning you can use funds from your Health Savings Account (HSA) or Flexible Spending Account (FSA) to cover the bill. This is true whether you’re using insurance for part of the cost or paying the full self-pay rate yourself. Using these accounts is a great way to pay with tax-advantaged dollars, and modern services like ChatWithDr also readily accept HSA and FSA payments.

Navigating Insurance Networks

Your insurance network is just the group of doctors and clinics your insurer has a pricing deal with. Sticking inside this network is the number one rule for keeping costs from spiraling.

What happens if I use an out-of-network urgent care center?

Going "out-of-network" means your insurance company has no pre-negotiated rate with that clinic. As a result, your insurer will cover a much smaller slice of the bill—if they cover any of it at all. You’ll almost certainly be on the hook for a much higher cost and might even have to pay the entire bill upfront.

To avoid this costly surprise, always check that a clinic is in your network before you go. You can usually confirm it in minutes on your insurer's website or with a quick phone call.

Comparing In-Person and Virtual Care Costs

The rise of telehealth has introduced a new, super-competitive price point for medical care, making it a powerful first choice for many common problems.

Is telehealth cheaper than an in-person urgent care visit?

For most common conditions, the answer is a huge yes. A typical self-pay urgent care visit can start at $100-$250 just for the consultation, and that's before any tests or treatments. In contrast, telehealth services often charge a single, flat fee—like $39.99—that covers the entire consultation, diagnosis, and treatment plan. By cutting out the overhead of a physical clinic, telehealth offers a seriously cost-effective first stop for non-emergency medical needs.

You can find more detailed answers to your questions on our Frequently Asked Questions page.

Do I have to pay for my urgent care visit upfront without insurance?

Yes, almost always. Urgent care centers typically require self-pay patients to pay for all services at the time of the visit. It’s how they can offer those discounted "prompt-pay" rates—it saves them the headache and cost of billing you later. You should plan on paying the estimated cost of your visit before you see the doctor.

Ready to skip the waiting room and get care on your terms? For a flat fee, ChatWithDr provides 24/7 access to board-certified doctors who can diagnose, treat, and prescribe medication right from your phone. Get started now at https://chatwithdr.com.

Related posts:

The 7 Best Online Doctor Services of 2025: A Detailed Review

The 7 Best Online Doctor Services of 2025: A Detailed Review  How to Get Medical Care Without Insurance Your Practical Guide

How to Get Medical Care Without Insurance Your Practical Guide  How much does urgent care cost? A Practical Guide to Bills and Savings

How much does urgent care cost? A Practical Guide to Bills and Savings  Decoding the Virtual Doctor Visit Cost for Smart Healthcare

Decoding the Virtual Doctor Visit Cost for Smart Healthcare  Difference Between Urgent Care and Emergency Explained

Difference Between Urgent Care and Emergency Explained